It may surprise many of our readers, but here in the U.S. the Federal Communications Commission (FCC) and the National Telecommunications and Information Administration (NITIA) are not the only agencies with a vital interest in trends impacting the availability of universal communications. In fact, in many ways, possibly the source of the most current information when it comes to gauging the trend of people going from wireline telecom service to wireless is actually the U.S. Centers for Disease Control and Prevention (aka, the CDC), who views basic voice connectivity as a national health issue worth tracking.

The CDC has just posted as part of its National Health Interview Survey Early Release Program the following report, Wireless Substitution: Early Release of Estimates From the National Health Interview Survey, July–December 2013. Authored by Stephen J. Blumberg, Ph.D., and Julian V. Luke Division of Health Interview Statistics, National Center for Health Statistics, the report not only has become a topic of discussion on the major news, but has the blogosphere abuzz as well.

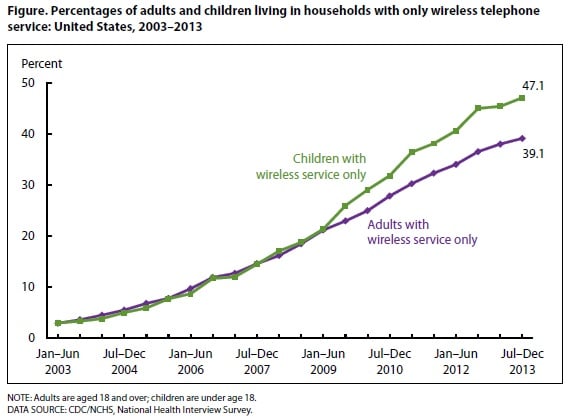

While the report has some interesting demographic data in it, and by all means is something you should read in its entirely since its 13 pages are mostly tables of data the CDC releases early so other parties can do some number crunching, the chart that created the stir is the one below:

Yes, you are reading it correctly, the number of U.S. households that are “wireless only” continues to inch up towards the 50 percent mark and the number of children with wireless service only is basically there.

The chatter on the Internet has been about a host of things including:

- Should wireless now be considered basic common carrier service and regulated as such?

- What does this mean for triple play services as to their bundling and pricing?

- What does this mean for the future of landlines, industry restructuring as cable companies, OTTs, CLECs and even traditional network service providers readjust to the ways in which U.S. consumers consume services as things like personal devices and their desirability of multi-screen experiences continues to explode?

- What does it say about the state of universal service that lower income people are the ones who represent the segment of the population with the highest percentage of wireless only households?

And, that is the short list.

The finding that can be seen in the most recent years on the chart that wireless only household adoption is slowing is the one that really got some juices flowing. Inquiring minds were hot on speculating as to whether this represented the fact that the addressable market of households will to cut the cord has been saturated or merely a pause in the action.

Those saying we have peaked argue that because of generational issues many people just do not feel comfortable without a wireline phone for emergencies. In addition, the contention is that economics, i.e., lower income people like the rest of us can’t live without our mobile phones but cannot afford to pay for a wireline and/or triple play in addition, and that market is saturated.

Those who say we are just resting and the trend of getting rid of wireline service will continue saying that demographics and psychographics belie the above conclusions. Plus, they say that as a result of LTE deployments, the installed base of mobile smart devices is getting long in the tooth and there is a massive replenishment coming that will help drive more interest, and reduce fears about less than terrific service (including issues regarding E-911), and hence the market will grow substantially.

Interestingly, also brought into play in all of this has been the implications of the entire shift away from how all of us in the U.S. consume entertainment services. Streaming video from likes of Netflix, Hulu, et al, has caused many people to disaggregate what once was triple play in favor of just Internet service. Where this comes in is that rational consumers rationing their total communications spend believe they can get by quite well with a mobile device and the Internet to meet all of their calling, entertainment and other interactions needs.

This latter observation is one to really watch closely. It adds fuel to the fire of those who think we are poised for impressive growth in households without wired phones. WebRTC, by the way, is an additional accelerant as calling from the web browser takes off. Plus, this is also a trend making cable operators crazy and upsetting the entire content delivery business as pressures mount for cable channels to be offered a la carte instead of in bundles. Indeed, it is not going to take too many streamed hits like Netflix’s House of Cards to give everyone pause as to what business model/packages will work best going forward.

Will wired telephony go away? My suspicion is that it will not, but it is certainly not going to be our father’s phone service, and how regulators decide what this century’s universal service is and how it gets paid for is going to play a huge role in all of this, despite the fact that regulatory lag is going to mean the market will likely decide long before policy makers.

Way back in the late 1970s and early 1980s as competition was just getting going in the wired business there was the notion of the “Primary Instrument.” What this meant was that as part of regulated basic service everyone should have a device and an affordable plan for connecting to the network. Who knows it might be time to dust off that notion with people designating their primary instrument and service for basic connectivity. In the meantime, don’t look for triple play to die soon, although it may die hard when the time comes, and wired voice as part of that Internet service in essence will exist if only as a loss leader.

Edited by

Maurice Nagle