A new report, “State of USF: New Rural Investment Challenges,” from telecom advisors Balhoff & Williams, LLC may be highlighting an instance of that old saying, “No good deed goes unpunished.” The report makes a rather compelling case that states must act promptly to determine how they will address a probable shortfall in funding for rural broadband and telecom services arising from the implementation of reforms to the Universal Services Fund in the form of the Connect America Fund (CFA).

The CFA, created as a result of now departed Federal Communications Chairman Julius Genachowski’s desire to overhaul the obsolete USF regime, in theory was designed to assure that the gap between people living in less densely populated areas had the same access to broadband services as their city friends. The question that Balhoff & Williams examined was whether the CFA would accomplish its goals without disturbing who would have to pay for what. In their view it does and the states are going to be the biggest losers.

“Our analysis suggests that service will falter in certain regions or significant incremental costs will have to be borne by customers, unless new sustainable and predictable support revenues are made available,” write the authors. Put simply, they believe the CFA is underfunded.

The reasons cited are that many rural areas will not receive support through the new programs. This is because they do not meet eligibility requirements or because of a belief that service providers will reject funding at the levels and terms and conditions offered by the government and walk away from high-cost customers, i.e., those in hard to reach places where population densities make service provisioning in their view prohibitively expensive. The authors say that, under this likely scenario, the states will have to make up the difference if services are to be provided.

It should be noted that there is a lot of data to back up these assertions. The 45-page report is filled with an explanation of the history of how we got here as well as charts that document why this underfunding is a near and present danger.

Some of the more interesting findings include:

- For CAF I, the carriers judged -- at least in 2012 -- the majority of the FCC’s initial funding to be short of the obligations imposed by the Commission. The result was that the carriers’ preliminary “commitments” were to invest based on a mere $115 million of the $300 million offered. It is our understanding that the carriers may choose to decline some of the $115 million as they further assess the obligations, although there are indications that the FCC may not allow reassessments.

- The FCC originally expected to begin funding CAF II by December 2012 with higher allocations in 2013. At this point, the FCC has not announced a definitive model nor does it have an announced set of obligations and eligible locations, although it appears that these are in process.

- The CAF II funding is for only five years, after which the FCC can reassign the obligation to an alternative carrier through an auction. However, funding for networks generally requires recovery over a longer horizon, as costs have typically been recovered over a period closer to 20 years. This disparity between funding and recovery mechanisms could cause the carriers to be more reluctant to accept the new obligations.

- Because the investment obligations could rise from 4 Mbps/1Mbps, according to the FCC, to 6 Mbps/ 1.5 Mbps, a rational carrier will assess a single network buildout so it will not have to return and upgrade the broadband plant. The analysis in the near term is likely to include assessing costs that assume the faster speeds, with the likelihood that the near-term CAF will not meet that higher cost threshold.

- Sixteen states have eliminated carrier of last resort obligations that require incumbent local telcos to offer phone service to all locations in their territory.

- Wireless is not an appropriate substitute for landline broadband because of usage caps. The authors calculate that the monthly mobile broadband cost for the median rural broadband user would be $120 to $165 and for the average user would be $300 to $400 based on AT&T and Verizon rates.

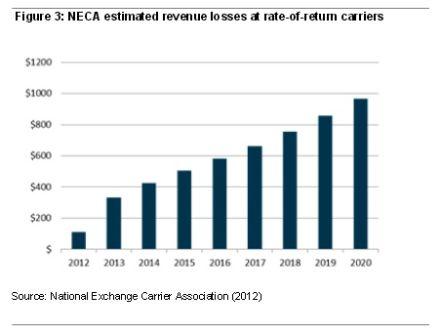

- Rate of return carrier revenue losses have been climbing because of reductions in inter-carrier compensation and other factors, according to data from the National Exchange Carrier Association. NECA estimates that rate of return carriers’ annual revenue decline will reach $1 billion by 2020.

- Revenue declines, combined with difficult-to-predict caps on today’s voice-focused Universal Service program and uncertainty about the CAF program, have sharply decreased rate of return carrier investment. The Rural Utilities Service, a key lender, was able to place its full loan portfolio every year Balhoff and Williams have been able to track until 2012, when borrowers drew down only 11.6 percent of the $690 million that was available.

- AT&T has said that there is no business case for deploying broadband to 25 percent of its local service territory.

- Just over half (26) states have state Universal Service programs. In addition, Vermont is considering such a program. Balhoff and Williams suggest that more states may need to adopt such programs in order to ensure that residents continue to receive communications services.

As to winners and losers, the authors state the following:

The FCC has stated that customers in denser regions will benefit from reduced prices and, in the future, customers in the CAF II funded areas will see improved and more sustainable access to broadband and voice services. In the near term, however, the biggest winners are the large diversified carriers, such as AT&T and Verizon. Because those two carriers account for nearly 50% of the long-distance market share in the U.S. and serve nearly two-thirds of the wireless subscribers, they are net beneficiaries of the reforms with cost savings larger than revenue losses. Sprint and T-Mobile are also clear beneficiaries as they have no local access revenues to lose but will benefit from lower intercarrier charges paid to local telecommunications companies.

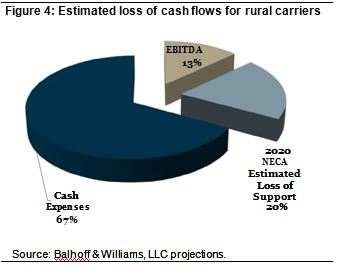

Customers in many high-cost regions will be the ultimate losers, as traditional investment-focused support is reduced going forward. By 2020, the price-cap carriers will no longer have access to significant levels of the support funding previously dedicated to investment in many of their high-cost areas. By the same point in time, we estimate that rate-of-return rural carriers will lose an estimated one-third of today’s federally-regulated intercarrier compensation (and related embedded support monies) and USF explicit support.”

This is not a pretty picture. The authors note that it actually understates the problem because this is not just about revenues but cash flows which as the figure below shows are going to be significant.

The old saying is that the bottom line is the bottom line. The authors conclude by saying: “States that wish to encourage and maintain universal access to voice and broadband services, therefore, will have to understand what is occurring related to support funding, as well as the policy issues when federal support is insufficient, and what realistic actions can be taken if universal service policy is to survive. The time is very short for those analyses, particularly if the states wish to partner with carriers and take advantage of the federal support programs.”

Given the political clout of states with significant rural populations, this report is going to cause a stir to say the least. In fact, do not be surprised if this becomes a major topic of discussion on June 18 when President Obama’s nominee to be the next FCC Chairman, Thomas Wheeler, starts his confirmation hearings. There are states’ rights jurisdictional issues that the next head of the Commission is going to have to deal with based on things like the end of carrier of last resort disappearing and what to do about the regulation of VoIP services in that context, along with the heat Senators are sure to feel from the governors of their respective states. If the numbers are correct, and there certainly appear to be based on the terms and conditions of CFA I and CFA II, this is a challenge that will not go away without it seems some kind of fine-tuning. Stay tuned.

Edited by

Rich Steeves